Homeowner Equity Surged in Q2

There was another big surge in the amount of equity on the balance sheets of American homeowners in the second quarter of this year. CoreLogic reports that the 4.3 percent gain in home prices over the past year sent home equity shooting up by 6.6 percent.

The report shows U.S. homeowners with mortgages (which account for roughly 63 percent of all properties) saw an average gain in equity from the second quarter of 2019 of $9,800. The collective nationwide increase was $620 billion.

This is especially important at this point, as equity may provide some insulation for homeowners during the pandemic. During the housing boom millions of buyers used low down payment mortgages and there was an epidemic of cash-out refinances, leaving many homeowners with little equity. When prices began to fall, millions fell quickly into negative equity, owing more on their mortgages than their homes are worth. This left them with little flexibility to refinance or sell their homes to get out of financial difficulty.

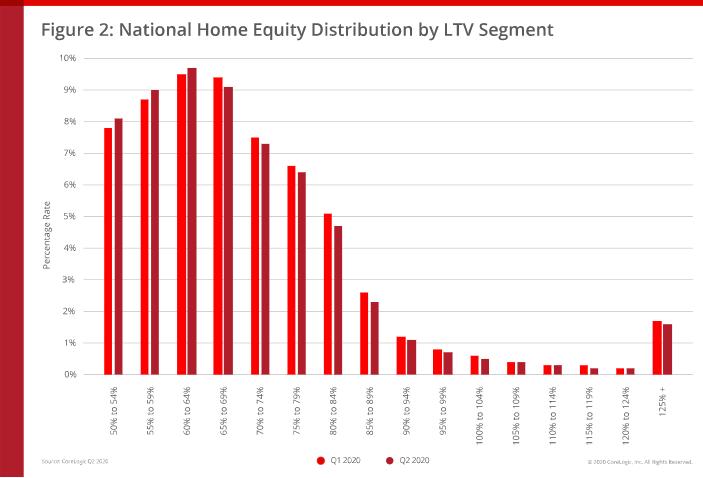

The number of mortgaged properties with negative equity decreased by 15 percent year-over-year in the second quarter of 2020 to 1.7 million homes with loan to value (LTV) ratios of 100 percent or more, 3.2 percent of all mortgages. There was a decline of 5.4 percent in underwater homes from the first to the second quarter of 2020.

The national aggregate value of negative equity was approximately $284 billion at the end of the second quarter of 2020. This is down quarter over quarter by approximately $0.7 billion, or 0.2 percent, from $285 billion in the first quarter of 2020, and down year over year by approximately $20 billion, or 6.6 percent, from $304 billion in the second quarter of 2019.

Despite a slowdown in April when the coronavirus began to spread, home-purchase activity remained strong in the second quarter of 2020 as prospective buyers took advantage of record-low mortgage rates. This, along with the seemingly perpetual inventory constraints helped drive home prices up and add to borrower equity through June. However, with unemployment expected to remain elevated throughout the remainder of the year, CoreLogic predicts price growth will slow over the next 12 months and mortgage delinquencies will continue to rise. These factors combined could lead to an increase of distressed-sale inventory, which could put downward pressure on home prices and negatively impact home equity.

"The CoreLogic Home Price Index registered a 4.3 percent annual rise in prices through June, which supported an increase in home equity," said Dr. Frank Nothaft, chief economist for CoreLogic. "In our latest forecast, national home price growth will slow to 0.6 percent in July 2021 with prices declining in 11 states. Thus, home equity gains will be negligible next year, with equity loss expected in several markets."

Borrowers with equity positions near the negative equity cutoff are most likely to move out of or into negative equity as prices change. Looking at the second quarter of 2020 book of mortgages, if home prices increase by 5 percent, 270,000 homes would regain equity; if home prices decline by 5 percent, 380,000 would fall underwater.

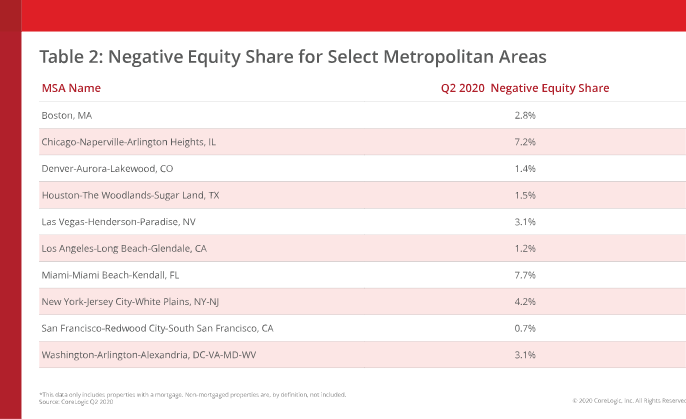

While national figures reflect a resilient housing market thus far into the recession, equity gains varied broadly on the local level. States with strong home price growth have continued to experience the largest gains in equity. This includes Montana, where homeowners gained an average of $28,900; Idaho, an average of $21,200 and Washington, $20,400. Meanwhile, New York, which was hit hard by the pandemic, experienced some of the lowest equity gains (averaging just $4,400) and highest negative equity shares in the second quarter of 2020.

"Homeowners' balance sheets continue to be bolstered by home price appreciation, which in turn mitigated foreclosure pressures," said Frank Martell, president, and CEO of CoreLogic. "Although the exact contours of the economic recovery remain uncertain, we expect current equity gains, fueled by strong demand for available homes, will continue to support homeowners in the near term."